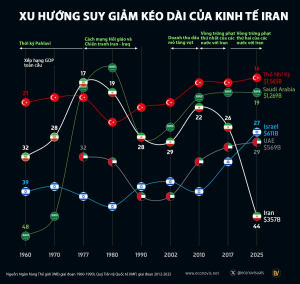

During the period from 1960 to 1976, Iran recorded an average economic growth rate of 10.8% per year. In 1977, one year before the Islamic Revolution, the country was the world’s 17th-largest economy.

At that time, Iran’s economic size was larger than that of Saudi Arabia (ranked 18th), Turkey (20th), the United Arab Emirates (32nd), and Israel (40th).

Following the Islamic Revolution and the eight-year Iran–Iraq war, Iran’s economy deteriorated sharply. As a result, by the late 1980s, Iran had fallen to 28th place globally, behind Turkey.

Between 2002 and 2010, a surge in oil revenues helped Iran improve its ranking from 29th to 22nd. However, strict U.S. and international sanctions quickly reversed these gains.

The first round of sanctions—mainly multilateral measures coordinated by the United States with the European Union (EU) and the United Nations (UN)—pushed Iran’s economy down to 26th place by 2017.

The second round of sanctions, reimposed and expanded by the United States from 2018 after its withdrawal from the Joint Comprehensive Plan of Action (JCPOA), contributed to Iran’s further decline to 44th place by 2025.

From 2011 to 2025, Iran’s gross domestic product (GDP) grew at an average rate of only about 1.6% per year.

According to analysts, Iran’s prolonged economic decline reflects the compounded impact of multiple factors, including international sanctions, political tensions, weak economic governance, domestic corruption, and the fiscal burden of Tehran’s regional interventions. These factors placed significant pressure on Iran’s growth over the 2012–2025 period.

Leave a Reply