According to Mr. Hung, being upgraded by FTSE Russell is just the starting point in the development journey of the Vietnamese stock market.

![]()

At the Cafef livestream with Securities organized by SSI Securities, Mr. Pham Luu Hung, Chief Economist and Director of SSI Research, commented that the decision to upgrade Vietnam’s market to a secondary emerging market by FTSE Russell has significantly helped “relieve” concerns from foreign investors, while clearly demonstrating the coordination capacity and flexible handling ability of the management agency throughout the preparation process.

He stressed that the issues that arose in the final stage were all resolved in a short time, thereby paving the way for the official upgrade announcement, which is very positive for the market.

Looking back on the journey of preparing for the upgrade over the past time, Mr. Hung said there have been many fundamental changes.

Since November last year, Vietnam has implemented a non-prefunding trading mechanism, followed by the issuance of a document eliminating the requirement for consular legalization in the account opening process for foreign investors, significantly shortening the procedure for entering the market.

In addition, Decree 155 has also been amended and supplemented with many important regulations related to listing activities, shortening the time from IPO to listing, and clarifying regulations on foreign ownership ratio.

Another highlight is the implementation of the KRX system, which is considered a “turning point” for the Vietnamese stock market. The chief economist of SSI shared that before the KRX system was put into operation, the level of skepticism of foreign investors about the possibility of implementation was even higher than the skepticism about whether Vietnam could be upgraded or not. However, after the system was successfully put into operation, transaction latency has decreased sharply, approaching that of countries in the region. This has significantly strengthened foreign investors’ confidence in the market.

Not only that, compared to many countries that have been upgraded before, Vietnam is certainly not at the bottom of the list. He believes that after being officially upgraded, the Vietnamese stock market will quickly rise to the middle group of emerging markets and has the potential to become one of the leading markets in the future when its scale and depth continue to improve.

The long-term attractiveness of Vietnam’s stock market

Asked whether investment funds tracking the frontier market index would sell when Vietnam is officially upgraded, Mr. Pham Luu Hung said this is unlikely to happen in the short term.

Currently, the number of funds using the FTSE Frontier index is not large, so the selling pressure is insignificant. Moreover, the time for Vietnam to officially take effect is quite long, until September 21, 2026.

” During this period of more than a year, if funds need to restructure their portfolios, they can completely do this slowly. With the relatively small scale of this fund group, the portfolio “rebalancing” will not create much pressure on the Vietnamese market ,” Mr. Hung pointed out.

Commenting on the attractiveness of the Vietnamese stock market in the coming period, Mr. Hung emphasized that the upgrade story is just one of many factors in the capital market development process.

In addition to meeting technical criteria, regulators and market participants are still working to increase market depth. One of the important solutions is to promote IPO activities. In fact, large IPOs such as TCBS have created a strong catalyst not only for securities stocks but also forecast to significantly improve liquidity in the entire market.

According to Mr. Hung, in the coming time, when more and more large-scale enterprises go public, along with the general development of the market, this will be an opportunity to attract more foreign capital. The upgrade helps Vietnam affirm that it has met the standards of an emerging market, but the long-term attractiveness also comes from many other factors such as the list of quality stocks, the story of economic growth or the excitement of new listing activities.

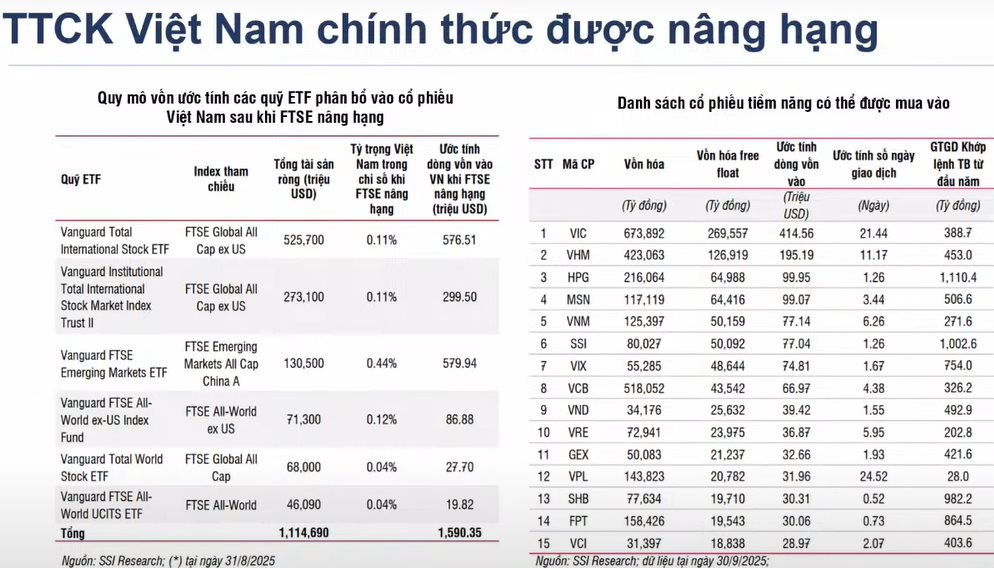

SSI estimates capital inflow of about 1.6 billion USD from passive funds when upgrading

The expert also noted that since the beginning of the year, foreign investors have sold a net of about $4 billion, which is much larger than the estimated $1.6 billion in capital inflow from passive funds when Vietnam is upgraded. “ If Vietnam can re-attract the capital withdrawn thanks to market reform and expansion, it will be a much bigger story than passive funds buying at the time of the upgrade ,” he emphasized.

According to Mr. Hung, being upgraded by FTSE Russell is just the starting point in the development journey of the Vietnamese stock market. The further goal is to be recognized as an emerging market by MSCI, thanks to which the scale of foreign capital flow can increase significantly.

If we imagine it on a “10-point scale”, the capitalization and cash flow when reaching MSCI standards will be at “10 points without any buts”. To move towards this, Vietnam is implementing the central clearing counterparty (CCP) model, which is a criterion not included in the FTSE framework but is an important condition to approach MSCI standards.

Leave a Reply