The global financial system constantly holds its breath over the threat of a U.S. government default. But there is an even more frightening scenario—a paradox so counterintuitive that it could collapse the entire system even faster than a default: the prospect of governments suddenly paying off all their debt.

A world drowning in debt

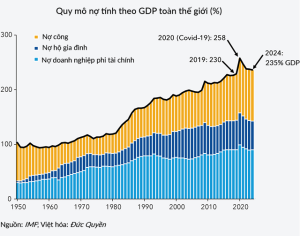

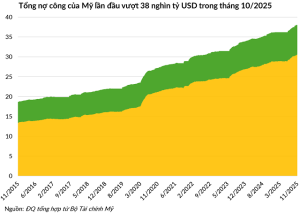

Public debt has become a permanent feature of the modern world. According to the Institute of International Finance (IIF) and the International Monetary Fund (IMF), total global public debt has exceeded 100 trillion USD. This figure is not only concentrated in the United States, which is burdened with more than 38 trillion USD in government debt.

Japan’s debt-to-GDP ratio stands at over 250%. In Europe, major economies such as Italy (nearly 145%) and France (115%) are also overwhelmed by debt.

The truth is that every country on Earth—from export powerhouses like Germany and China to oil-rich kingdoms like Saudi Arabia—is a massive debtor. This raises the question: If everyone is borrowing, then who is actually the lender? And how can a system that appears so fragile and precarious continue to function?

A tangible fear of default

For decades, U.S. public debt has been more than just a number—it has been the foundation of the global financial system. U.S. Treasury bonds are considered “risk-free assets,” the safest haven for global capital. The belief that “the United States will always pay its debts” is an axiom that requires no proof.

Therefore, the prospect of the U.S. government failing to repay even a small portion of its debt when due would be a catastrophe, shattering the core trust that has maintained global financial order for the past 80 years.

Global liquidity would freeze, banks would stop trusting one another, and a financial crisis worse than 2008 could unfold. The world briefly glimpsed this specter in 2011 when a political standoff over the debt ceiling pushed the U.S. to the brink of default, leading to the first-ever downgrade of its AAA credit rating.

The danger of default is real. But it overshadows an even more terrifying scenario.

The money-creation machine built on government bonds

Imagine a seemingly impossible scenario: governments around the world somehow possess enough cash to pay off all their public debt.

Instead of celebration, the financial world would plunge into a crisis even worse than a default. Why?

The answer lies in the true nature of public debt in the modern economy. Government debt, or government bonds, is not simply a borrowing agreement—it has evolved into a foundational asset used to create money.

Most of the “money” in today’s economy is not physical currency printed by central banks, but credit created by private banking systems. And this credit-creation machine only works if it has one critical fuel source: high-quality collateral.

U.S. Treasury bonds—along with, to a lesser extent, other sovereign bonds—are that fuel. The value of a bond lies not only in its face value, but in its usefulness as collateral to leverage even more money through the money markets.

Every night, a bank holding 1 billion USD in Treasuries doesn’t simply wait for interest payments. It brings those bonds to the money market, uses them as collateral, and borrows a huge amount of cash.

That cash is then used to lend to other businesses, generating new credit. This loop—amplified by rehypothecation—allows a single bond to underpin multiple layers of transactions. The result: a 1-billion-USD bond might be supporting a “credit tower” worth tens of billions of dollars.

Paying off the debt: Pulling the plug on the money-creation engine

Now let’s return to the hypothetical scenario of governments paying off all their debt. This would trigger a catastrophic domino effect because paying off debt is not “injecting money” into the system—it is “withdrawing the license to create money.”

When the government repays 1 billion USD to a bank, the bank receives 1 billion USD in cash—but the 1-billion-USD bond disappears permanently. Its disappearance means the foundation of an entire credit tower collapses. All repo-market loans secured by that bond are suddenly without collateral.

The bank may hold 1 billion USD in cash, but 10 billion USD in credit built on that bond has just evaporated. The net result is a sudden contraction in money supply and liquidity. The money-multiplication engine stops. Systemwide liquidity freezes because there is no longer reliable collateral. Banks stop lending to each other. The financial system becomes paralyzed.

Paying off the debt would destroy the very structure that allows the economy to function.

Debt is never meant to be fully repaid

In the modern world, public debt is not designed to be eliminated. It is designed to be rolled over—governments issue new bonds indefinitely to repay old ones.

“Perpetual debt” is not a new invention. The model began in 1694 when England, exhausted from war with France, borrowed money from merchants at 8% interest forever, with no maturity date. The English state used its taxation power to guarantee repayment and established the Bank of England to administer the debt.

Today, rolling over debt has become standard policy. Governments borrow not only to finance wars, crises, healthcare, and education, but also—crucially—to pay the interest and principal on old debt.

The global financial system operates on faith that this rollover machine will never stop. A government default is certainly bad, but paying off all debt is not the desired outcome either.

What we call the government’s “debt” is, in fact, the financial system’s “asset.” Debt is the foundation of an architecture built entirely on trust. And in that architecture, stability does not come from erasing debt, but from the assurance that debt will exist forever.

Leave a Reply