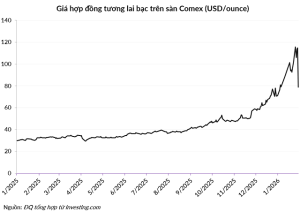

After a 31% plunge on January 30, 2026, pessimism and fear have gripped the silver market. However, long-term investors need to step back and assess whether the broader supply–demand and macroeconomic picture for silver has fundamentally changed. At this point, investors essentially face two choices: exit the market in fear and regret, or take advantage of lower prices and bet on a coming commodity supercycle.

Silver had a stellar year in 2025, surging 140%. In January 2026, even after the brutal 31% collapse on January 30, silver still ended the month with a 12% gain. No one can predict exactly when or how sharply silver will fall, but the recent crash was not entirely surprising. Silver has long been notorious for its extreme volatility, largely due to the relatively small size of its market.

Right now, uncertainty dominates as investors question whether silver’s uptrend has ended—and what comes next.

To answer that question, it is worth revisiting the forces that have driven silver to successive highs over the past few months. Were these gains fueled solely by speculative capital, or were they underpinned by solid fundamentals? If those fundamentals remain intact, then short-term volatility may simply be turbulence on a long flight—uncomfortable, but not catastrophic.

Chronic shortages, rapidly depleting inventories

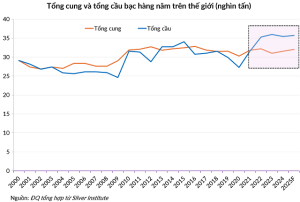

The world is consuming silver far faster than it can be mined, with supply falling short of demand for five consecutive years. According to data from the Silver Institute, the cumulative supply deficit from 2021 to 2025 totaled nearly 800 million ounces (around 25,000 tonnes). To cover this shortfall, the world has been steadily drawing down above-ground inventories.

Stocks at major exchanges such as the LBMA (London) and Comex (New York) have fallen by about 70% since 2021. This situation resembles a household that must continually sell off furniture just to cover daily expenses—the world is edging closer to an “empty house” scenario when it comes to silver.

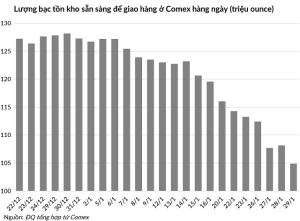

Comex data show that in January 2026 alone, inventories declined by 43.5 million ounces (nearly 1,400 tonnes), equivalent to about 10% of the year’s starting level. Registered silver—metal that is actually available for delivery—fell nearly 18% during the month, to less than 105 million ounces.

And this downward trend shows no sign of slowing. January is typically a seasonal lull, yet January 2026 saw nearly 9,900 contracts standing for physical delivery—an unusually high number. Open interest as of January 30 stood at 148,000 contracts, equivalent to 740 million ounces of silver. If just one-seventh of those contracts demanded physical delivery, Comex’s registered inventories would be completely exhausted.

On the supply side, global mine production has essentially stagnated, growing by only 1–2% in both 2024 and 2025. The root cause lies in geology: roughly 72% of the world’s silver is mined as a by-product of copper, lead, and zinc operations. This means miners cannot simply ramp up silver output when prices rise unless demand for base metals increases as well. Silver supply is therefore extremely price-inelastic.

Adding to the strain, China— which controls 60–70% of global silver refining capacity—began enforcing strict silver export restrictions on January 1, 2026.

While this move is intended to safeguard strategic resources for Beijing’s technological ambitions, it effectively removes a massive source of supply from the global market. The result is an unprecedented supply shock, forcing Western industries to compete fiercely for an ever-shrinking pool of available silver.

Industrial and defense demand: No choice but to buy

If supply is tightening, demand is simultaneously surging. Silver is not only a monetary metal like gold; it is also a critical input for the modern economy.

AI and data centers’ thirst for silver: Data centers and AI infrastructure require ultra-high-performance, low-latency electronic connections. Silver, the most electrically conductive metal, is irreplaceable in semiconductors, connectors, and switching equipment.

In December 2025, the Silver Institute released a startling forecast: electricity demand from the information technology sector by 2030 is expected to be 52 times higher than today, implying massive silver demand for power transmission infrastructure and hardware to support this energy-hungry expansion.

Green energy devours silver: The solar photovoltaic (PV) industry remains a major “black hole” for silver consumption. Solar technology is shifting from older PERC cells to next-generation, higher-efficiency technologies such as TOPCon and HJT. Crucially, these newer technologies use 30% to 120% more silver than their predecessors.

Demand for silver from the PV sector is expected to continue setting new records, despite ongoing—yet largely unsuccessful—efforts to find effective substitutes.

Electric vehicles (EVs) also represent a powerful source of demand, as a single EV uses roughly twice as much silver as a traditional internal combustion engine vehicle. The Silver Institute forecasts that EV-related silver demand could reach 200–250 million ounces per year by 2030, accounting for nearly a quarter of global silver supply.

Inelastic demand: The key factor supporting silver prices over the long term is the price inelasticity of industrial and defense demand. A $50,000 electric vehicle or a guided missile system costing millions of dollars contains only tens to hundreds of dollars’ worth of silver.

As a result, even if silver prices double or triple, companies such as Tesla, Samsung, or Lockheed Martin will still be forced to buy silver to keep production lines running. Corporations do not care about candlestick charts or RSI indicators—they care about having enough physical material to prevent billion-dollar factories from shutting down. This is the “hard demand” that underpins the market.

The macro backdrop: Cheap money and the debt spiral

Beyond its industrial role, silver is reclaiming its status as a monetary asset amid eroding confidence in fiat currencies.

U.S. public debt is approaching $39 trillion, with annual budget deficits nearing $2 trillion. In this context, the Federal Reserve faces a classic dilemma: keep interest rates high to fight inflation and risk government insolvency due to soaring debt service costs, or cut rates to support the government and risk reigniting inflation.

History suggests governments invariably choose to print money and inflate their way out of debt. An environment of cheap money and a weakening U.S. dollar is the most fertile ground for rising gold and silver prices.

Bullish forecasts

Citigroup has dubbed silver “gold on steroids” and forecasts prices reaching $150 per ounce within the first three months of 2026. The bank has outlined an even more optimistic scenario: if the gold-to-silver ratio returns to its 2011 low of 32, silver could reach $170 per ounce. Notably, silver already hit a high of $121 per ounce in January 2026.

Michael Widmer, an analyst at Bank of America, has offered a wide but still bullish price range of $135 to $309 per ounce. While $309 may sound extreme, it is not implausible when adjusted for inflation relative to silver’s 1980 peak.

Signals from the U.S. Mint: Recall that on January 14, 2026, the U.S. Mint—the sole producer of official coinage for the world’s largest economy—temporarily halted sales of popular collectible coins such as the American Silver Eagle due to “rapidly rising input costs.” The Mint has since resumed sales, but at prices that raise eyebrows.

In early January, a one-ounce collectible coin was priced at $95. After sales resumed in late January, the price jumped to $173 per coin—an 82% increase and more than double the post-crash Comex silver price following the January 30 sell-off.

Of course, U.S. Mint collectible coins are intricately crafted and produced in limited quantities, so they typically command a substantial premium over standard bullion. Still, an abrupt 82% price hike to $173 in a single adjustment suggests that the U.S. Mint is deeply concerned about rising silver input costs in 2026 and has raised prices to avoid operating at a loss.

Leave a Reply